- New York

- London

- Glasgow

- Paris

- Singapore

ESG Mastery: Transforming CSRD Obligations into Brand Excellence

8 January 2024

As of January 2024, the Corporate Sustainability Reporting Directive (CSRD) introduced mandatory sustainability reporting for larger European corporate entities, defined as those with €40 million turnover, €20 million in assets or more than 250 employees (source: the Autorité des marchés financiers (AMF), the French financial markets authority).

Although an EU directive, companies listed or operating in the EU will have to comply, with few exceptions based on net turnover for foreign entities without a branch or subsidiary in the EU. By 2029, an estimated 50,000 companies will have to produce a sustainability report compared to around 10,000 today.

Reports for these listed entities, and those already subject to the Non-Financial Reporting Directive (NFRD), will be due in 2025. In 2026, other large companies that are not currently subject to the NFRD (and may not be listed) will be due to report. Listed small and medium enterprises (SMEs) will be required to report in 2027, with the remainder of SMEs due to report by 2030.

True, this legal obligation sounds like another onerous reporting requirement. However, at Copylab, we believe it is an excellent opportunity for asset management companies to differentiate themselves with clear communication around their understanding and commitment to sustainability issues. Furthermore, we believe companies should view such reports as a marketing tool rather than just a tick-box exercise to satisfy compliance.

In this article, we outline which companies could become liable for CSRD and the positive implications of yet another ESG report. We also explain the type of sustainability data that will be required by your company and how you could include it in your marketing strategy to gain incredible traction with your client base.

So, are you CSRD-ready?

What requirements are covered by the CSRD?

Just like the EU Taxonomy and Sustainable Finance Disclosure Regulation (SFDR), the CSRD is part of the EU Financial Framework Regulations. The CSRD’s objective is to expand and replace the NFRD and make ESG reporting systematic to meet a pressing need for consistency and more in-depth analysis.

- From 2024, a larger band of companies will become eligible until 2029, marking the inclusion of smaller businesses. Those with a headcount of just 10+ employees may be required to report should they meet a turnover or balance sheet threshold in the EU.

- Each company has a timeline of 12 months to produce its initial corporate sustainability report. Updates will then be published every four years.

- There will be a standardisation of the reporting through the European Sustainability Reporting Standards (ESRS) that were voted on over the summer and explained in the paragraph below.

- All data are to be verified by a third party, such as a statutory auditor or an independent body. Each country has until the end of the year to choose an auditing benchmark.

- All reports are to be published in digital format.

- Sustainable reporting is now a subsection of corporate management reporting.

- The company’s entire value chain falls under the sustainable reporting framework.

What will your new ESG content look like? | Presentation of the ESRS standards.

Harmonisation of existing standards.

One of the goals of the CSRD is to harmonise ESG reports that currently follow a variety of standards, guidelines and legal frameworks across the world. To achieve this, the European Commission (EC) asked the EFRAG (the European Financial Reporting Advisory Group) to examine the following existing standards:

- The GRI (Global Reporting Initiative)

- The SASB (Sustainability Accounting Standards Board)

- The TCFD (Task Force on Climate-related Financial Disclosures)

- Other international frameworks, such as the IFRS (International Financial Reporting Standards)

Based on lessons learned and best practices from these existing requirements, the EFRAG drafted the new ESRS to ensure that sustainability information is easily navigable and reported per the CSRD. Additionally, the ESRS aims to achieve a balance between enabling as much comparability as possible and allowing flexibility in recording information pertinent to specific sectors.

A good reason to get in touch with your ESG (or compliance) teams.

We think this regulatory change is a great opportunity to ensure your firm stands out. To achieve this, we recommend you start a conversation with your ESG or compliance teams, as they may not have spotted this great branding opportunity. Below we have listed the questions you might want to ask:

- Is your company currently following any of the old guidelines listed above?

- What does your ESG team’s reporting schedule look like? There might be scope to move to more consistent reporting regimes with the introduction of this effort to harmonise sustainability reporting.

- Could your ESG team repurpose some material from sustainability reports they are currently working on?

And if you are new to this – for example, your firm now needs to complete a TCFD report for the first time – we can help!

Breakdown of the ESRS components:

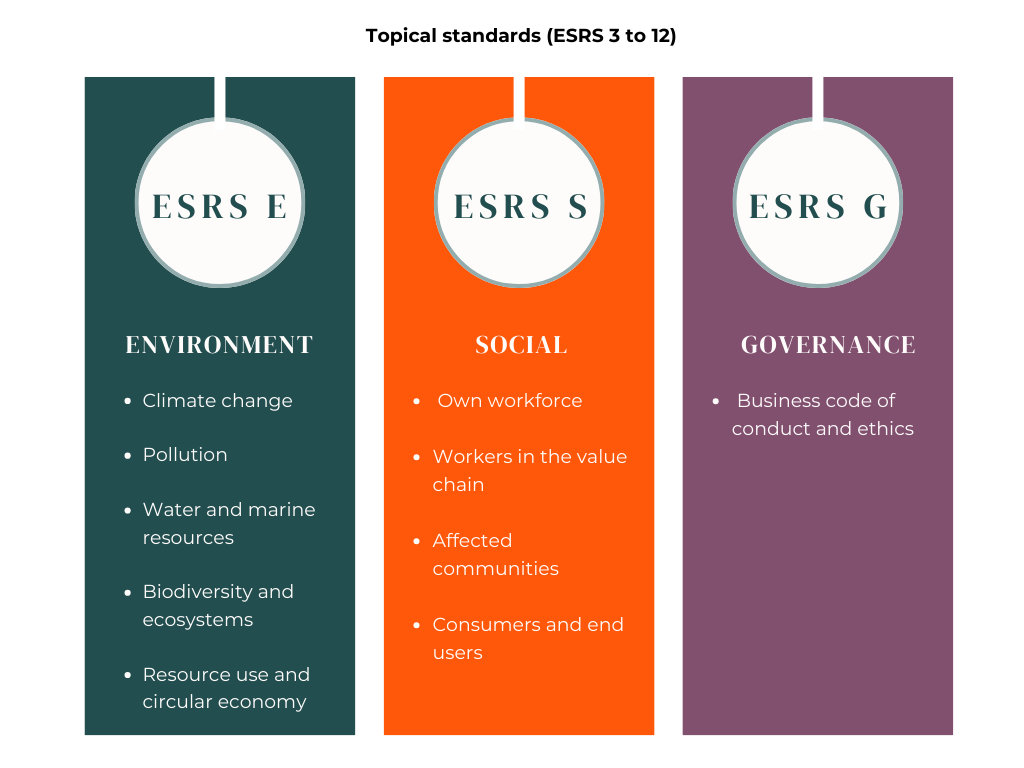

The ESRS framework is composed of 12 standards that are applied across all industries to promote consistency. The first two cover the general requirements and overarching general disclosures (ESRS 1 and 2) while the other ten (ESRS 3 to 12) are topical. Here’s a quick walkthrough:

1. General requirements and disclosures (ESRS 1 and 2):

- ESRS 1 are general requirements based on the principle of “double materiality”. Companies will need to assess the financial and socio-environmental impact they have on their environment as a first step. Then they will need to assess the opposite – in other words, how they are impacted financially by people and their environment.

This exercise is designed to identify which topical ESRS standards (3 to 12, presented below) the company should report on.

{kind=link}

ESRS 2 are in line with the TCFD and the International Sustainability Standards Board. The general disclosures present four pillars of reporting for each of the ESRS topics as identified during the double materiality assessment:

- Governance

- Strategy (definition and outcome of the double materiality assessment)

- Impact, risk and opportunity management

- Metrics and targets

2. Topical standards (ESRS 3 to 12):

How do we go from data gathering to impactful storytelling?

At a time when the financial services industry is still the subject of harsh criticism, with greenwashing accusations in some cases, this new set of legal requirements could be a blessing in disguise – an opportunity to restore trust. Your data collection efforts and the transparency of your reporting can reach beyond legal reporting compliance and be a unique tool to boost the power of your brand.

Sustainable reporting is an ideal opportunity for your company to show its willingness to be fully accountable while taking your branding image to the next level. At Copylab, we have extensive expertise in sustainable development reporting, so if you are uncertain about how to get started to present your company’s story with authenticity, please contact us.

Here are six ways you can turn this accountability exercise into your true story:

- Prioritise your ESG communications strategy with your firm’s centralised ESG team. There are 7 key questions you need to ask your ESG team to best provide context to your CSRD report.

- Lend your facts a voice. The financial services industry has been heavily criticised for fact-spinning and making empty promises. However, the amount of data needed for the CSRD report allows you to avoid this by giving you the scope to provide greater clarity.

- Use storytelling to showcase your company’s values. Organising your sustainability data in a way that tells the story of your challenges and opportunities while also presenting your milestones and achievements is a unique way to testify to your company values. Make sure you define your tone of voice to resonate with your clients.

- Define your long-term strategy and corporate vision. The forecasts and projections needed for this new reporting can help your company define its long-term strategy, which may position you as a leader in the industry. Have you discussed this with your ESG team?

- Differentiate yourself through thought leadership. During the data-gathering process, you and your ESG team may identify innovative or impactful business practices that could help you stand out among your peers.

- Consider document design. Why not use graphic media (infographics, for example) to achieve a sterling reading quality and turn your report into an attractive brochure to compensate for the demanding and fact-intensive content?

Sustainable reporting is an ideal opportunity for your company to show its willingness to be fully accountable while taking your branding image to the next level. If you are uncertain about how to get started to present your company’s story with authenticity, please do not hesitate to get in touch.